For many years, the U.S. institutional shareholder community has largely influenced policy and practices behind the scenes, which was particularly the case with the largest fund managers.

With the evolving regulatory landscape and more clients holding their asset managers accountable for their voting records on governance, compensation and environmental, social and governance (ESG) matters, major institutional shareholders have stepped forward to play a significant leadership role in shaping the discussion on corporate governance and executive compensation matters.

An increasing number of issuers are now directly engaging with their major shareholders on governance matters, with more engagements now involving board members.

The ever-present shadow of activist shareholders has certainly been a motivator in cases — 456 companies were targeted by activists in 2016, up from 417 in 2015, according to Activist Insight.

While investor approaches and agendas can vary widely, in early 2017 a coalition of 16 of the largest U.S. and global investors (Investor Stewardship Group, a collective of the largest investors that represent $17 trillion in assets under management), launched its “Framework for U.S. Stewardship and Governance.” This framework outlined investor expectations about corporate governance practices in U.S. issuers and investment principles (as it relates to proxy voting and engagement guidelines) for investors. This is a voluntary code but could become quite meaningful with the new administration having signaled a shift in direction for the regulatory landscape.

With this context, we welcome the opportunity to get the latest perspectives on executive compensation and governance matters from representatives of two leading asset managers: Yumi Narita, vice president of BlackRock Inc., and Anne Sheehan, director of Corporate Governance and Aeisha Mastagni, portfolio manager of California State Teachers’ Retirement System (CalSTRS). (The interviews have been condensed and edited.)

What are your compensation priorities for the next year?

BlackRock: As a fiduciary, all engagements with companies are undertaken with the goal of protecting and enhancing the long-term economic interests of our clients, and this long-term value mindset is fundamental to all we do.

This is particularly true when it comes to compensation. Executive pay policies should link closely to the company’s long-term strategy and goals. We want to see executives rewarded for delivering sustainable returns over a longer time horizon and not, for example, receiving a compensation windfall due to a short-term surge in stock prices. We remain focused on ensuring that companies disclose their strategies for the long term and compensation plays a very large role with aligning shareholder value creation. A company should have balance and prioritization between input metrics that are within a company’s control relative to output metrics, such as earnings per share or total shareholder return.

We think that today’s increased scrutiny on pay has helped eliminate some of the worst compensation practices. However, it’s come at the expense of two things: increased complexity and homogeneity of pay plans. We think increased complexity can potentially result in higher compensation with less transparency while homogeneous pay-plan designs may ultimately fail to align pay with a company’s strategy.

Companies should ask whether their incentive plans are truly incentivizing and are in the best interests of long-term investors.

CalSTRS: We are looking for companies to articulate their strategy and how it supports the pay program. We want to ensure there is a consistent linkage between long-term objectives and compensation paid to executives. Our focus is typically on outliers — companies that have the most egregious pay practices or the least pay-for-performance connection. We understand that compensation is more art than science, but we’re looking for an appropriate balance. For most of the companies where we are voting against their say on pay, it is an aggregate of several red flags. It’s never just one issue. It’s things like: a lack of pay for performance, duplication of metrics for the short term and long term and a high ratio of CEO pay compared to the other named executive officers (NEOs). Any type of award outside the regular pay program is going to get an incredible amount of scrutiny from us. We have yet to hear an argument that has convinced us on these awards outside of a regular pay plan. This suggests that an existing pay plan isn’t working or is giving extra pay to what is intrinsic to an executive’s duties.

Incorporating strategic, environmental or social objectives into incentive plans is one way of reducing focus on short-term financial results. But a concern from issuers is that shareholders may find them too soft or subjective. Any reaction?

CalSTRS: Generally, we don’t tell companies which specific metrics to use, though we believe there is typically two or three value-driving metrics for most industries. Industry-specific metrics do make a lot of sense to us. We are looking for more granularity, especially for subjective metrics. We want to know why a metric was chosen, how it links to the long-term strategy and how it is measured. For example, innovation is a metric that makes sense for tech companies, but it can be hard to quantify beyond the number of new products released. However, a tech company could explain how R&D is being spent appropriately and what the process is for determining projects that go forward versus projects that you pull the plug on. We just don’t want you throwing good money after bad, so it’s about explaining that to shareholders.

BlackRock: I’d frame the question differently because it assumes that environmental or social objectives do not necessarily tie into something quantifiable and measurable. If an environmental/social objective is material to the company and can be used as a metric, we wouldn’t have an issue with it being included in an incentive plan. As for a metric that may be too subjective, for example “leadership quality,” we believe should be part of any executive job description.

The average length of a Compensation Discussion and Analysis (CD&A) is now 80 pages. How do you see the current state of CD&A disclosure?

BlackRock: We see the CD&A as an effective communications tool, not just a regulatory compliance filing compiled by a company’s legal team. We encourage companies to go beyond what’s mandated by the regulators, such as having multiyear realizable pay numbers that might help better communicate their compensation philosophy. Companies should ensure that what they include in the disclosure effectively communicates what they’d like to say to investors.

It is also important to note that length does not necessarily improve a CD&A. In fact, we view the CD&A’s executive summary as important to helping us understand how a company’s pay philosophy and long-term corporate strategy impacts compensation.

CalSTRS: The short answer is that they are long. To some extent, the length is a result of how complicated pay programs are. We look at the summary compensation table but we also use other tools to help us find that link between pay and performance. Realizable pay makes more sense to us philosophically than realized pay, which includes an element of the decisions made by the executives to exercise or hold different securities. Given the many ways realizable pay can be calculated, we use statistical tools to enable an apples-to-apples comparison across companies rather than the realizable disclosure provided by a company.

What has your experience with engagement been like?

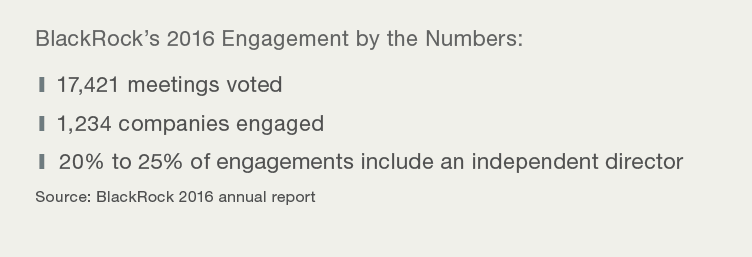

BlackRock: Engagement has evolved quite a bit over the past few years. I remember speaking at a conference in 2011 to a room full of investor relations professionals, where I brought up the idea of shareholders engaging with independent directors. The room got very, very quiet.

We recognize directors are busy people, so ultimately not every engagement necessarily requires a director, but we will specify when we would like to have a conversation with them.

We recently published our engagement priorities on the BlackRock Investment Stewardship website (blackrock.com) and I would strongly encourage companies to review this document. Among other broad governance themes, our 2017–2018 engagement priorities include human-capital management, where we lay out how companies are working to support and engage a stable workforce and how boards oversee the management team in this area.

When it comes to compensation, if we identify a company with a pay-for-performance disconnect, we carefully read through its public disclosures looking for a detailed explanation as to why this pay structure makes sense for the company. We may also engage directly with compensation committee members, as they are ultimately accountable to investors for setting executive compensation.  We may vote against compensation committee members as well as the say-on-pay proposal where a company hasn’t connected all the dots in terms of corporate strategy, long-term shareholder value creation and incentive plan design.

We may vote against compensation committee members as well as the say-on-pay proposal where a company hasn’t connected all the dots in terms of corporate strategy, long-term shareholder value creation and incentive plan design.

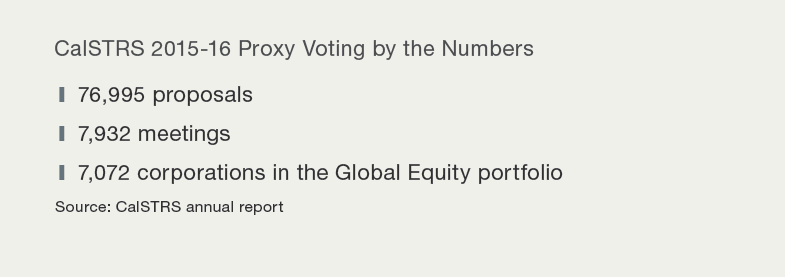

CalSTRS: Engagement is up exponentially. Inbound calls and the number of directors in our engagements are also up. We think it is a good thing. It’s important for us to make sure that directors hear the message directly from shareholders and they are now more willing and available to do it. That’s their job. But we don’t need to engage every year nor have a director at every engagement. Companies shouldn’t be insulted when we determine that there is no need to do a call.

As a large index shareholder, we are going to be invested in these companies for a long time. At CalSTRS, we believe that starting with quiet engagement and discussion is the most constructive approach. It builds a relationship and helps us explain our approach,  how we view the company’s governance, how we see the investment. Engagement is also critical in our understanding of the long-term strategy and how the company and board operate.

how we view the company’s governance, how we see the investment. Engagement is also critical in our understanding of the long-term strategy and how the company and board operate.

Shareholder activists have used concerns about compensation as a door opener for some boards that may have lost their way. Any advice for companies facing this particular challenge?

BlackRock: The activist landscape has changed. Today, activists increasingly use the vocabulary of governance to make their case to mainstream investors. Broadly speaking, companies and boards should be open to at least listening to what an activist has to say. We do understand that in certain situations an activist can catalyze board refreshment, which may be needed, or can help create some long-term value for the company. Other times, an activist’s ideas may have already been thoroughly reviewed and dismissed by a board or otherwise not be aligned with the long-term economic interests of all shareholders.

When considering whether to engage or settle with an activist, it is important to us that board and management teams balance an open mind with the courage of their convictions. We encourage companies to reach out to investors directly to make sure they understand investor perspectives over any third party that might purport to know our views.

Companies should listen carefully to the concerns that their large shareholders are raising. Investors often signal concerns by the way they ask questions or prioritize certain topics. Companies and boards should be paying attention to these nuances and ask themselves if there is something they are missing or if there are areas for improvement.

CalSTRS: Our advice to the companies would be not to lose their way on compensation for the executives as they are setting the pay packages. If they feel they are at risk, chances are they are. So, they should hold the mirror up to themselves and ask “Do we have the right structure?”

Any final thoughts for HR professionals responsible for executive compensation?

BlackRock: Companies too often reference proxy advisory firms when they engage with us. It’s important to note that while we use proxy advisory data, we do not necessarily follow their recommendations. At BlackRock, we publish voting guidelines by region, an annual report on engagement, as well as case studies. Instead of focusing on a proxy adviser recommendation, focus on what investors are saying and doing.

CalSTRS: A company’s workforce is one of its best assets. Given the importance of all the issues related to human capital, it would seem that there are a lot of companies that could use more experience and knowledge in the boardroom on how these incentive programs drive behavior.

The other piece of advice would be to scan the landscape for trends, innovations and practices issues that shareholders are investing in. Don’t become isolated by only talking to the folks inside the company. Get out and test drive your program against best market practices. What are some new innovative ways of looking at compensation?